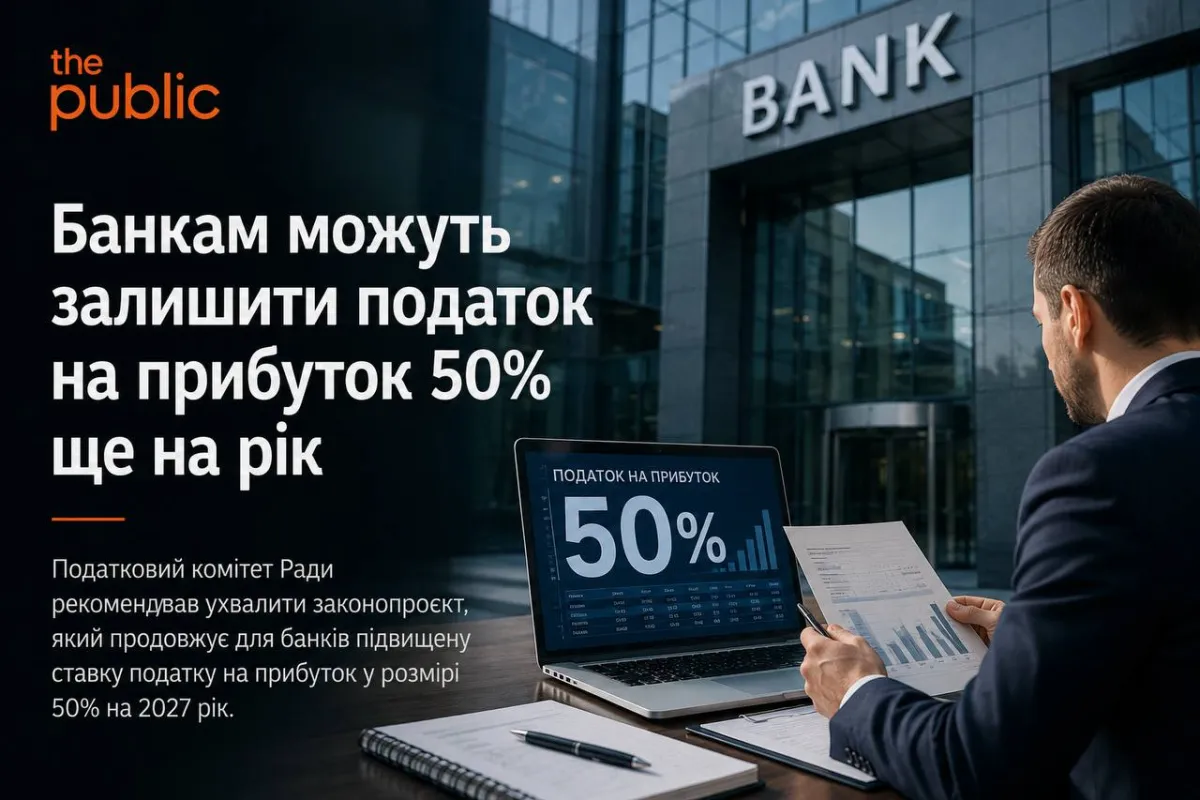

Banks may be allowed to retain a 50% income tax rate for another year

This was announced by Danylo Getmantsev, Chair of the Verkhovna Rada Committee on Finance, Tax and Customs Policy. What changes are being proposed

Draft Law No. 15262 provides for the extension of the increased corporate income tax rate of 50% for banks into 2027.

The bill also prohibits banks from reducing their pre-tax profit by the amount of losses from previous periods.

How much revenue is expected

According to the Ministry of Finance’s estimates, the adoption of the bill could generate 50 billion hryvnias for the consolidated budget based on the results of the 2027 tax periods.

Which provisions does the bill amend

The document proposes amendments to paragraph 73 of subsection 4 of section XX “Transitional Provisions” of the Tax Code of Ukraine.

For the 2026–2027 tax periods, the corporate income tax rate for banks is to be 50%.

During this period, banks will also be unable to apply sub-clause 140.4.4 of the Tax Code. In other words, they will not be entitled to reduce their pre-tax financial result by the amount of losses carried forward from previous years.

When will banks be able to offset losses

It is proposed that losses incurred by banks from 1 January 2026 to 31 December 2027 be taken into account to reduce future profits only from 1 January 2028.

This means that, for the duration of the increased rate, banks will effectively be unable to use certain tax mechanisms to reduce their tax base.

What the National Bank says

The National Bank of Ukraine has opposed the extension of the increased rate.

The NBU states that the banking sector has already exhausted its financial reserves following the payment of the extra tax in 2023 and 2024.

The regulator also warns that extending the 50% rate could reduce lending to the economy.

What risks does the NBU see

According to the National Bank’s assessment, the expected additional fiscal impact of around 20 billion hryvnias could result in a loss of 200–300 billion hryvnias in potential lending capacity.

The NBU explains this by the fact that profit remains the main source of bank capitalisation, as dividend payments are limited for most institutions.

What is the tax burden on banks

The National Bank also draws attention to the uneven distribution of the tax burden.

The banking sector already pays income tax at a rate of 25%, whilst the standard rate for other sectors of the economy is 18%.

According to the NBU, banks account for around 11% of all tax revenues to the budget, although the sector’s share of GDP is approximately 2.9%.

Follow us on Telegram